Massive Financial Irregularities Uncovered in Kerala's Co-operative Banking Sector

Government data has exposed staggering financial irregularities amounting to over Rs 1,582 crore in Kerala's co-operative banking sector between 2015 and 2025. This revelation highlights profound governance failures within a network of institutions that manage the savings and credit needs of millions of residents across the state.

Karuvannur Bank Scandal Triggers Statewide Outrage

At the heart of this crisis lies the Karuvannur Service Co-operative Bank, where irregularities worth Rs 125.83 crore were detected. This scandal, involving inflated collateral values, dubious loans, and internal collusion, sparked widespread public anger and intensified calls for comprehensive scrutiny of the entire co-operative sector. The Karuvannur episode served as a tipping point, compelling the government to confront long-suspected structural weaknesses in co-operative lending and oversight mechanisms.

High-Level Committee Recommends Systemic Safeguards

In response to the escalating crisis, the government appointed a high-level committee to investigate the irregularities and propose systemic safeguards. The panel's report paints a bleak picture of how procedural lapses, a lack of professional expertise, and regulatory complacency facilitated large-scale fraud, not only in Karuvannur but potentially across the broader co-operative credit system.

The committee identified serious failures in loan processing, particularly in collateral valuation and appraisal, which allowed vested interests to siphon off funds by artificially inflating property values. Warning that similar frauds could recur elsewhere, the panel recommended mandatory inclusion of professional directors in all loan-issuing co-operatives under Section 28(1G) of the Co-operative Societies Act.

Stricter Loan Protocols and Property Valuation Reforms

For loans exceeding Rs 10 lakh, the committee proposed a stricter regulatory regime. This includes mandatory project reports, construction plans, and cost estimates where applicable. Such proposals should be examined by a committee comprising professional directors and the bank secretary, with loan disbursal linked to verified project milestones through binding circulars issued by the registrar.

Property valuation emerged as a major concern. To curb inflated assessments, the committee recommended establishing a state-level panel of qualified valuers. Collateral for loans above Rs 10 lakh should be accepted only based on certificates issued by these empanelled professionals.

Audit Weaknesses and Digital Security Concerns

Audit practices also came under sharp criticism. While audits are conducted regularly, weak follow-up mechanisms have significantly reduced their effectiveness. The report called for deficiencies to be clearly recorded, reviewed by managing committees, and rectified through compliance reports, with taluk-level assistant registrars held responsible for enforcement.

The committee further highlighted irregularities in Monthly Deposit Scheme (MDS) transactions due to the absence of uniform rules, recommending standardized conditions and accounting practices. It also warned about potential manipulation of digital records and advocated for uniform software across primary societies, stronger security protocols, and mandatory staff rotation every two years from sensitive posts.

Broader Sector Vulnerabilities and Lack of Safety Nets

The report noted that the Kerala Co-operative Risk Fund Scheme, 2008, provides no compensation to depositors affected by fraud or financial irregularities, leaving victims of scandals like Karuvannur without any safety net.

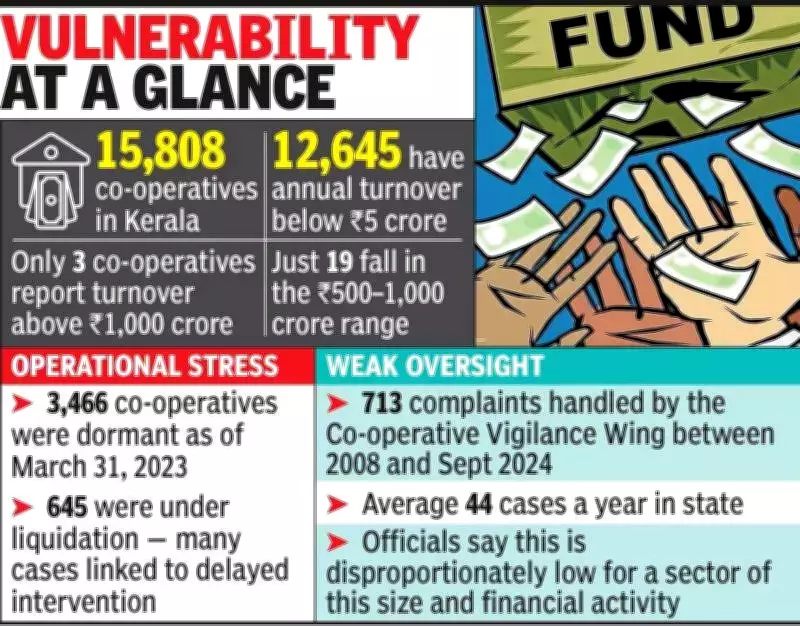

The broader vulnerability of the sector is starkly evident. Kerala has 15,808 co-operatives, with 12,645 reporting an annual turnover below Rs 5 crore. Only three have turnovers above Rs 1,000 crore, while just 19 fall in the Rs 500–1,000 crore range, indicating a vast base of financially fragile institutions.

As of March 31, 2023, 3,466 co-operatives were dormant and 645 were under liquidation—outcomes the study suggests could often have been avoided with timely intervention. Between 2008 and September 2024, only 713 complaints were handled by the co-operative vigilance wing, averaging 44 cases per year. Officials describe this figure as disproportionately low for a sector of this size and financial scale.