India presents a puzzling economic picture as 2025 draws to a close. On one hand, the domestic economy is showcasing remarkable strength, but on the other, the national currency is touching unprecedented lows against the US dollar. This divergence highlights how global financial currents can sometimes overshadow robust domestic fundamentals.

The Tale of Two Realities: Booming Economy vs. Falling Rupee

The latest official data reveals that India's Gross Domestic Product (GDP) expanded by a robust 8.2% in the July-September quarter of 2025. This impressive growth is supported by multiple factors. Inflation, a key concern for any economy, remains under control, staying within the Reserve Bank of India's (RBI) comfort band of 2% to 6%.

Equity markets reflect this optimism. The benchmark Nifty 50 index has climbed nearly 10% since the start of January 2025. Furthermore, the primary market is experiencing a historic boom, with Initial Public Offerings (IPOs) raising a staggering sum of over ₹2 lakh crore this year alone.

The Currency Conundrum: A Record Low Despite Strengths

In stark contrast to these positive indicators, the Indian rupee has been on a persistent downward trajectory. On December 4, 2025, the currency weakened to a historic low of 90.35 against the US dollar. This represents a significant depreciation of 6.7% since January 2025, a performance that unfortunately crowns the rupee as the worst-performing currency in Asia during this period.

This creates a clear paradox: a fundamentally strong economy is accompanied by a steadily weakening currency. The explanation lies not within India's borders, but in the complex arena of international finance.

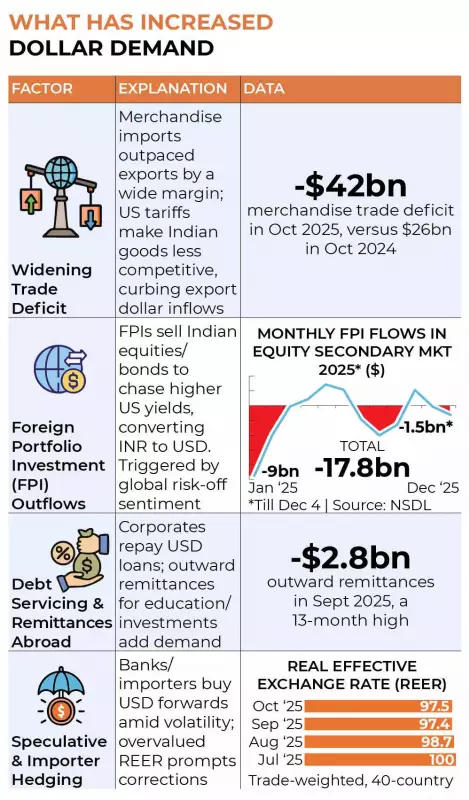

Global Turbulence Overpowers Domestic Momentum

The primary reason for the rupee's weakness is a persistent imbalance between the demand for and supply of US dollars within the country. Global investors, facing uncertainty and seeking safe-haven assets, often flock to the US dollar. This strengthens the dollar globally and puts pressure on emerging market currencies like the rupee.

Several key global factors contribute to this scenario:

- High US Interest Rates: The US Federal Reserve's monetary policy, often maintaining higher interest rates to combat inflation, makes dollar-denominated assets more attractive, pulling capital away from markets like India.

- Geopolitical Risks: Ongoing international conflicts and tensions fuel risk aversion, prompting investors to move funds to perceived safer destinations.

- Strong Dollar Outflows: There can be increased outflows of dollars for imports, debt repayments, or foreign investment by Indian companies, which adds to the demand pressure.

In essence, the domestic strengths of high GDP growth, controlled inflation, and a bullish stock market are being overpowered by these powerful global headwinds. The RBI actively manages the currency to prevent volatile swings, but it often cannot completely counter sustained global trends favoring the dollar.

Implications and the Road Ahead

A weaker rupee has mixed consequences. It makes imports, like crude oil and electronics, more expensive, contributing to input cost inflation. For companies with foreign currency debt, repayment becomes costlier. However, it also provides a boost to exporters and sectors like information technology (IT) services, which earn in dollars.

The current situation underscores the deep interconnectedness of the global economy. India's strong macroeconomic fundamentals provide a crucial buffer, but the rupee's fate is partially tied to external factors beyond direct control. The focus now is on whether domestic growth can continue to attract long-term foreign investment, which could eventually improve dollar inflows and support the currency.