ITAT Ruling Brings Relief to Cryptocurrency Traders in Tax Dispute

In a significant decision that could provide relief to thousands of cryptocurrency traders across India facing income tax demands, the Income Tax Appellate Tribunal (ITAT) in Ahmedabad has ruled in favor of an individual taxpayer. The tribunal ordered the deletion of additions made by an assessing officer to the taxpayer's income, citing inconsistent application of standards by the tax department.

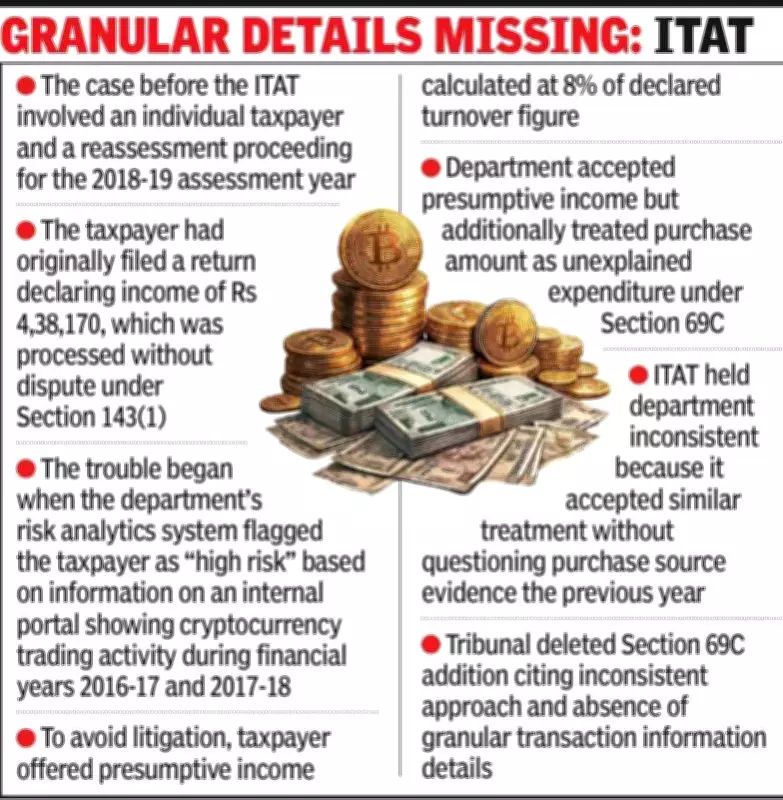

Background of the Case

The case involved a reassessment proceeding for the assessment year 2018-19. The taxpayer had originally filed a return declaring an income of Rs 4,38,170, which was processed without dispute under Section 143(1) of the Income Tax Act. However, the department's risk analytics system later flagged the taxpayer as "high risk" based on internal portal information showing cryptocurrency trading activity during the financial years 2016-17 and 2017-18.

Data indicated purchases of Rs 17,52,838 and sales of Rs 29,01,111 for the financial year 2017-18. A summons was issued seeking transaction details, but no response was recorded initially. The department then initiated proceedings under Section 148A, concluding that income had escaped assessment and issuing a reassessment notice under Section 148.

Taxpayer's Response and Department's Actions

During reassessment, the taxpayer disputed the lack of specific transaction-level particulars, such as coin names, broker details, dates, quantities, and gain or loss computations. To avoid prolonged litigation, the taxpayer offered presumptive income at 8% of the reported sales turnover, proposing Rs 2,32,089 on sales of Rs 29,01,111 for the year under consideration.

Sulabh Padshah, a chartered accountant involved in the case, explained, "The taxpayer pointed to the prior year's reassessment, where the department accepted a similar 8% presumptive approach on crypto sales without making any separate addition for the purchase side."

Despite accepting the offered presumptive income on sales, the assessing authority additionally treated the purchase amount of Rs 17,52,838 as unexplained expenditure under Section 69C and applied a special tax rate framework linked to such deemed income. The first appellate authority upheld the reassessment, citing failure to substantiate the source of investment and lack of documentary evidence linking purchases and sales.

ITAT's Decision and Implications

On further appeal, the ITAT noted that reassessment for both years was triggered by the same category of information and handled by the same assessment unit. The tribunal found that the department had accepted presumptive income in the earlier year without questioning the purchase source but took a contrary position in the subsequent year by invoking Section 69C.

The tribunal also observed that the underlying information relied upon lacked granular transaction details. Holding that this inconsistent approach was unjustified, the ITAT deleted the addition made under Section 69C and allowed the appeal.

Padshah added, "Finance Bill 2022 brought specific mechanisms for taxation of Virtual Digital Asset (VDA), applicable from April 1, 2022 onwards. This decision will be helpful in many cases where assessees engaged in frequent VDA trades before 2022, and the department is taxing them at a special rate of 60% under Section 69. Here, the assessing officer accepted trading activity as business activity, allowing tax at normal rates, and the tribunal upheld this, following principles of consistency and natural justice."

This ruling underscores the importance of consistent tax treatment and may set a precedent for similar cases involving cryptocurrency transactions prior to the implementation of specific VDA taxation rules.