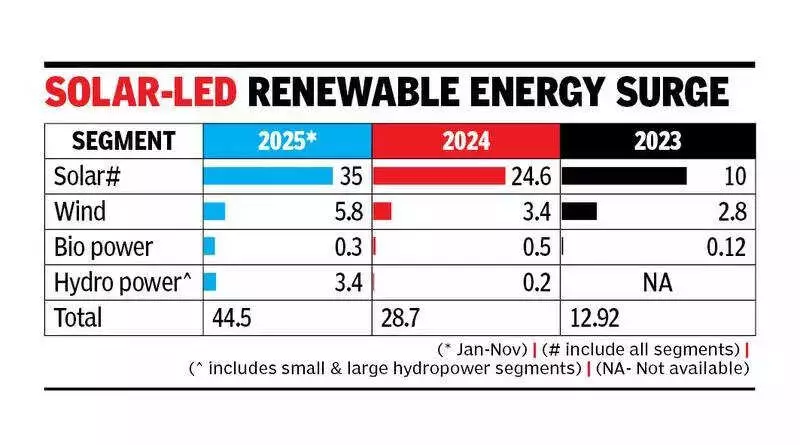

In a landmark achievement for the nation's green transition, India's renewable energy sector has shattered records in the current calendar year. Preliminary figures indicate that the country added a staggering 44.5 gigawatts (GW) of new capacity to the grid in just the first eleven months of 2025, setting a historic high for annual installations. This surge marks a dramatic acceleration from the approximately 28.7 GW added in the entirety of 2024.

Solar Power Dominates Unprecedented Growth

The monumental expansion has been overwhelmingly led by the solar power segment. Between January and November 2025, solar energy contributed a massive 35 GW to the grid, a significant jump from the 25 GW added in the previous year. This growth has propelled India's total renewable energy capacity, excluding large hydro projects, to 204 GW as of November 30, 2025, representing a robust 26% increase since the start of the year.

A detailed breakdown of the solar sector reveals that ground-mounted installations were the primary driver, accounting for about 26 GW of the new capacity. The rooftop solar segment made a substantial contribution of 7 GW, while hybrid projects and off-grid installations added the remainder. On the state front, Rajasthan continues to lead the nation with 36 GW of installed solar capacity, followed by Gujarat (25 GW), Maharashtra (17 GW), and Tamil Nadu (12 GW).

Wind Power Revival and Overall Capacity Mix

In a welcome development, the wind energy sector has also shown strong signs of revival. During the same 11-month period, it added approximately 6 GW of new capacity, its highest annual addition in recent years, breaking out of a previously subdued phase.

As a result of this combined growth, India's total installed renewable energy capacity stood at an impressive 254 GW as of November 2025, according to data from the Union Ministry of New and Renewable Energy. This portfolio comprises solar (133 GW), wind (54 GW), bioenergy (11 GW), small hydro (5 GW), and large hydro, including pumped storage, which accounts for 50 GW.

Sustained Momentum and Competitive Economics

The sector's momentum shows no signs of slowing. Reports indicate that an additional 135 GW of renewable capacity is currently under various stages of implementation or tendering, promising continued expansion. Crucially, the economic case for clean energy remains stronger than ever.

Tariff competitiveness is a key highlight, with record-low bids for utility-scale solar projects continuing in the range of Rs 2.44 to Rs 2.55 per kilowatt-hour (approximately $29–$31 per megawatt-hour). This trend, confirmed by analysts at IEEFA, underscores the sustained and growing cost advantage of clean energy technologies over conventional sources, making the green transition not just an environmental imperative but an economic one.

This record-breaking year solidifies India's position as a global leader in renewable energy adoption, showcasing a scalable model of how rapid decarbonisation can be achieved while maintaining economic viability.