Kolkata's Premium Residential Market Enters High-Velocity Growth Phase

Kolkata's premium residential market, encompassing properties priced between Rs 1.9 crore and Rs 5 crore, is transitioning into a period of accelerated activity characterized by increased project launches, faster unit absorption, and remarkably stable pricing. According to the comprehensive 2025 NKlusive report, this dynamic shift signals a robust, demand-driven expansion rather than a speculative bubble, reflecting strong consumer confidence and developer optimism in the city's high-end real estate segment.

Supply Expansion and Developer Confidence

The calendar year 2024 concluded with 26 premium residential projects actively operating in Kolkata. Building on this foundation, the market witnessed the introduction of 10 new launches in calendar year 2025, elevating the total to 36 live projects. This substantial increase serves as clear evidence of growing developer confidence in the sustained demand for properties within the Rs 2 crore to Rs 5 crore price bracket.

Marketable supply experienced significant growth, rising from 3,731 units in CY24 to 4,291 units in CY25. During this period, developers introduced 1,940 new premium units to the market. Geographically, south Kolkata maintained its dominant position, commanding a substantial 58% share of the city's premium residential supply. East Kolkata followed as a strong secondary corridor with a 20% share, reinforcing south Kolkata's status as the primary consumption zone for premium properties while highlighting the east's emergence as a complementary premium market.

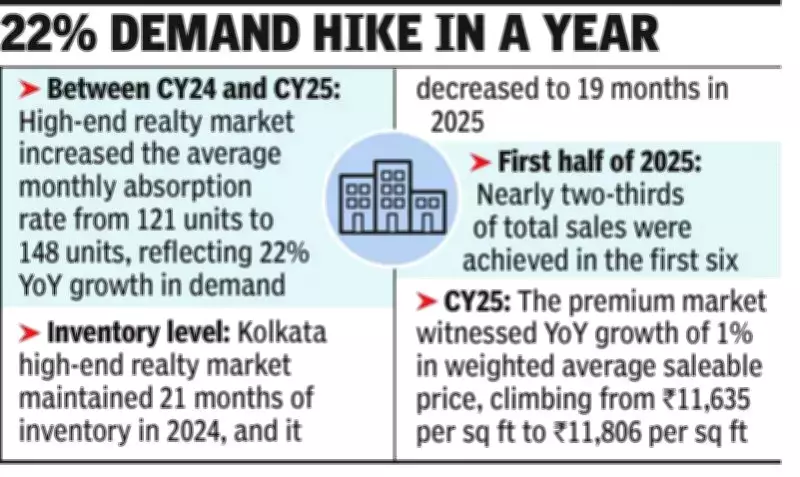

Strong Sales Performance and Absorption Rates

Despite the increased supply, sales performance remained exceptionally strong throughout the reporting period. In calendar year 2024, developers sold 1,355 premium units, representing 36% of the available supply. The following year saw even more impressive results, with 1,666 units sold, accounting for 39% of the supply. This translated to a remarkable 23% year-over-year growth in sales, which notably outpaced the 14% year-over-year growth in supply.

This divergence between sales growth and supply expansion clearly indicates that consumer demand is accelerating faster than new inventory additions. While unsold inventory did experience a 10% year-over-year increase, the market demonstrated improved liquidity by converting a larger percentage of available supply into actual sales. Monthly average absorption rates showed positive momentum, climbing from 121 units in CY24 to 148 units in CY25.

The market exhibited a pronounced front-loading of demand, with 65% of calendar year 2025 sales occurring during the first half of the year. This pattern suggests that buyers are acting earlier in the purchasing cycle, particularly for credible project launches and properties located in scarce micro-markets where availability is limited.

Price Resilience and Market Fundamentals

Premium pricing demonstrated remarkable stability with only mild upward movement. The weighted average saleable price increased by a modest 1% year-over-year, rising from Rs 11,635 per square foot in CY24 to Rs 11,806 per square foot in CY25. The key takeaway from this pricing data is the market's evident resilience: despite a substantial 14% jump in supply, prices did not soften, suggesting genuine end-user depth and significant brand-led pricing power among reputable developers.

This growth appears to be driven more by strategic product positioning, location scarcity, and developer credibility than by broad-based market inflation. The market is simultaneously expanding in breadth through more projects and units while improving in speed through higher absorption rates and increased sales share, all while maintaining disciplined pricing with only minimal increases.

Market Composition and Consumer Preferences

While south Kolkata continues to serve as the volume anchor for premium supply, emerging areas like New Town and the Bypass–Ruby corridor are gaining increasing prominence. The strongest market momentum remains concentrated in branded, well-located projects that benefit from scarcity advantages, particularly during the first half of the calendar year.

In terms of unit configuration, 3BHK apartments emerged as the highest-selling category in calendar year 2025. While both 3BHK and 4BHK units recorded identical sales of 607 units each in CY24, the following year saw 866 3BHK units sold compared to 685 4BHK units. This shift in preference highlights evolving consumer priorities within the premium segment.

Sushil Mohta, President of Credai West Bengal, commented on the underlying trends: "Rising disposable income and evolving aspirations are driving homebuyers toward premium residences. The share of homes priced above Rs 1.5 crore in Kolkata's overall sales basket has grown faster than in most other metropolitan cities across India."

The Kolkata premium residential market's current trajectory reflects a healthy, demand-led expansion supported by strong fundamentals, strategic development, and evolving consumer preferences that favor quality, location, and developer reputation over speculative investment opportunities.