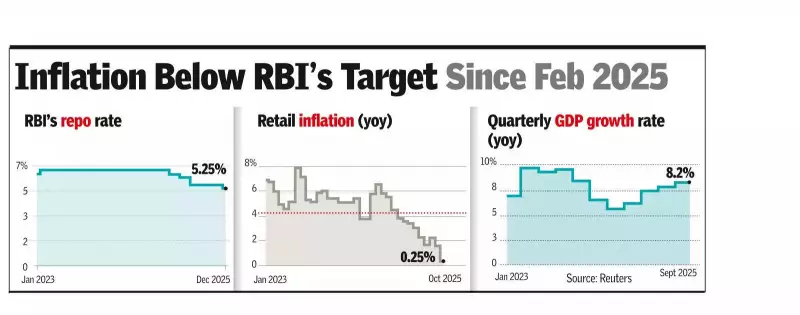

In a significant move to bolster economic growth, the Reserve Bank of India (RBI) announced its first reduction in the key policy rate in over a year on Friday. The Monetary Policy Committee (MPC) decided to lower the repo rate by 25 basis points, bringing it down to 5.25%. This decision is poised to make borrowing cheaper, potentially pushing home loan rates to their lowest levels in years.

Policy Shift and Economic Optimism

The central bank's decision marks a pivotal shift, supported by a substantial liquidity injection of nearly ₹1.45 lakh crore into the financial system. This boost comprises ₹1 lakh crore in bond repurchases and a 3-year dollar-rupee swap worth $5 billion. While maintaining a neutral monetary policy stance, the RBI expressed strong confidence in the Indian economy's resilience. Governor Sanjay Malhotra highlighted that despite global headwinds, domestic activity has remained robust.

The RBI sharply revised its growth projection for the fiscal year 2025-26 (FY26) upwards to 7.3% from an earlier estimate of 6.8%. Concurrently, the inflation outlook for FY26 was cut dramatically to 2% from 2.6%, with moderating food prices playing a crucial role. The central bank noted that underlying inflationary pressures are even softer when the volatile impact of precious metals is excluded from recent data.

Immediate Impact on Borrowers and Banks

The rate cut is expected to transmit quickly to the credit market. For home loan borrowers, this is welcome news. Several public sector banks currently offer home loans at around 7.35%. With the repo rate reduction, these rates are anticipated to fall to approximately 7.1%.

This decline will have a tangible effect on monthly budgets. For instance, on a ₹1 crore home loan with a 15-year tenure, the reduction could lower the monthly equated monthly installment (EMI) by roughly ₹1,440. However, for new borrowers to access these lower rates, banks may need to sharply cut deposit rates or accept narrower margins, creating a complex dynamic where recent floating-rate borrowers might benefit more than new applicants.

Non-banking financial companies (NBFCs) are likely to see faster transmission of the rate cut to their borrowing costs, providing quicker relief to sectors like truck financing, rural entrepreneurship, and MSMEs. Umesh Revankar of Shriram Finance termed the policy a "significant enabler" for last-mile finance.

Growth Trajectory and External Resilience

The RBI's optimism is backed by recent economic data. The Indian economy expanded by 8.2% in the July-September quarter of the current fiscal year, following a 7.8% growth in the April-June quarter. For the ongoing fiscal year, the RBI estimates GDP growth at 7% for the third quarter and 6.5% for the fourth quarter. Growth for the next fiscal year (FY27) is forecast at 6.7%.

Governor Malhotra credited factors like GST rate reductions and improved monsoon prospects for supporting demand. On the external front, he stated the sector remains steady despite foreign institutional investor (FII) withdrawals and weakness in merchandise exports, cushioned by robust services exports and remittances. India's foreign exchange reserves, standing at a substantial $686 billion (over 11 months of import cover), provide ample buffer against global volatility, even as the rupee trades around 89.84-90 per US dollar.

The RBI's move comes at a time when major central banks like the US Federal Reserve and the European Central Bank have paused their tightening cycles, raising expectations of global easing in 2026. However, strong domestic macroeconomic indicators, including a decades-low CPI inflation of 0.25% in October, provided the primary impetus for the Indian central bank's action.