Mumbai ITAT Delivers Landmark Ruling on Capital Gains Exemption Claims

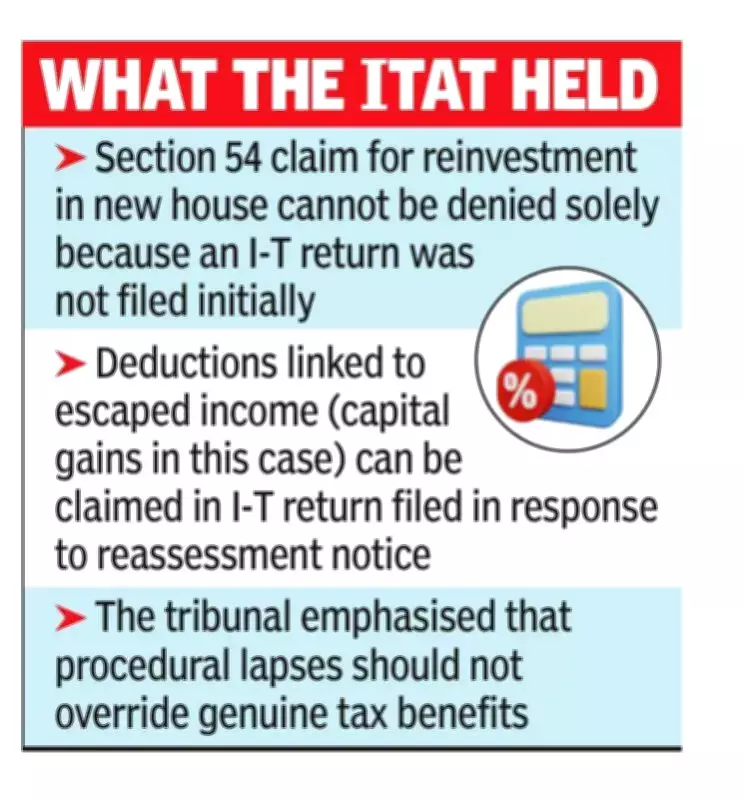

In a significant decision that strengthens taxpayer rights, the Mumbai bench of the Income Tax Appellate Tribunal (ITAT) has ruled that a claim for capital gains exemption under Section 54 of the Income Tax Act cannot be denied solely because the taxpayer did not file an original income tax return at the outset. The tribunal emphasized that such claims must be allowed if made during reassessment proceedings, provided they are directly connected to the income under scrutiny.

Case Background: The M Sheikh Matter

The ruling emerged from the case of individual taxpayer M Sheikh, who had not filed an original income tax return under Section 139(1) but subsequently filed one in response to a reassessment notice issued under Section 148. In this belated return, Sheikh disclosed long-term capital gains from the sale of a residential property and claimed an exemption of Rs 49 lakh under Section 54, based on reinvestment in another residential property.

Section 54 of the Income Tax Act provides that long-term capital gains from the sale of a residential property are exempt to the extent reinvested in purchasing another residential property within the prescribed timeframe. This provision aims to encourage investment in housing while providing tax relief to individuals.

Lower Authorities' Rejection and ITAT's Intervention

The assessing officer initially rejected Sheikh's exemption claim, citing the absence of an original tax return. This decision was later upheld by the commissioner (appeals), creating a procedural barrier that threatened to deny substantive tax benefits.

However, the ITAT bench took a different view, clarifying that while reassessment proceedings cannot revisit issues unrelated to escaped income, they do permit taxpayers to make claims directly connected to such income. The tribunal noted that the capital gains in question constituted the very income that had escaped assessment, and the Section 54 claim was intrinsically linked to computing that income.

"Therefore, it could not be treated as a fresh or unrelated claim barred in reassessment proceedings," the ITAT stated in its ruling.

Legal Precedents and Procedural Flexibility

The ITAT referenced earlier judgments establishing that Section 54 does not mandate filing an income tax return by the prescribed due date as a condition for claiming exemption. The tribunal emphasized that claims made in returns filed pursuant to reassessment notices cannot be rejected merely due to delay or absence of an original return.

Accordingly, the ITAT set aside the orders of the lower authorities and remanded the matter back to the income tax officer for fresh adjudication. The tribunal directed that Sheikh's eligibility for Section 54 exemption be examined on merits and allowed if statutory conditions are satisfied.

Expert Analysis: Substantive Rights Over Procedural Lapses

Tax experts have welcomed the ruling as reinforcing a crucial principle: procedural lapses, such as non-filing of an original return, should not defeat substantive tax benefits when the claim is otherwise valid and directly linked to income brought to tax in reassessment proceedings.

This decision provides important clarity for taxpayers who may have missed original filing deadlines but have legitimate claims for exemptions. It ensures that technicalities do not override the substantive provisions of tax law designed to provide legitimate relief.

The ruling also serves as a reminder to tax authorities to focus on the merits of claims rather than procedural technicalities, particularly in reassessment scenarios where the income itself is under examination.