Global trade tensions and the urgent push for clean energy have thrust a once-overlooked mineral into the spotlight: bauxite. As traditional supply chains face disruption, one Indian company, Ashapura Minechem, is capitalizing on a strategic pivot to West Africa, resulting in a dramatic surge in its market value. Its share price has soared by approximately 100% in the last six months and 89% over the past year. The central question for investors is whether this remarkable rally has a solid foundation for the future.

The Global Bauxite Crunch and Guinea's Rise

The global mining sector is undergoing a fundamental transformation. Growth is no longer solely measured by output volume but by secure access to critical resources. Geopolitical friction, tariff disputes, and evolving trade policies are forcing a redesign of international supply chains, placing a premium on resource security. Within this complex landscape, bauxite—the primary ore for aluminium—has become a strategically vital commodity.

Export restrictions from key suppliers, depleting reserves in established mining regions, and skyrocketing demand from the clean energy sector have converged to create a structural deficit. Guinea, holding an estimated 30 to 50 billion tonnes of bauxite reserves, has emerged as the world's most reliable source. This is perfectly timed with an accelerating global demand for aluminium, driven by infrastructure projects, electric vehicle production, and renewable energy installations. In India alone, aluminium demand is projected to more than triple by 2030.

Ashapura's Integrated Strategy: From Bentonite to Bauxite Powerhouse

Ashapura Minechem, founded in 1982 as a bentonite specialist, has meticulously built a diversified platform spanning mining, manufacturing, and trading. Its product portfolio now includes bauxite, kaolin, bleaching clay, silica, and iron ore, serving a B2B clientele across sectors like fibreglass, paints, cement, and oil & gas.

In India, bentonite and related minerals remain the core, contributing 45.2% of the FY25 turnover. The company is strengthening this base with two new mines in Kutch, expected to support 300,000 tonnes of annual dispatches. Its bleaching clay segment, commanding a 70% share in India's premium market, and the export-driven kaolin business further solidify its domestic standing.

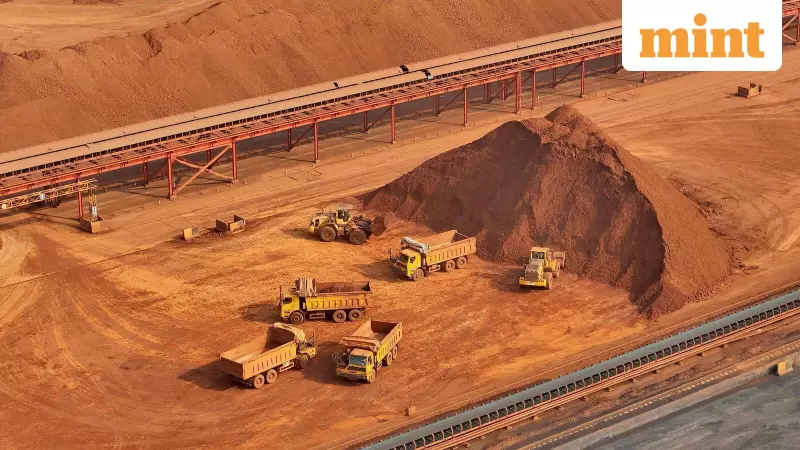

However, the true growth engine lies overseas. While bauxite contributes just over 7% to consolidated turnover, it is the critical volume driver for Ashapura's international ambitions, centered entirely in Guinea.

Mastering the Supply Chain in Guinea

Ashapura has gone beyond mere mining in Guinea to establish a fully integrated, end-to-end operational model. This provides immense control and cost advantages. The company operates three captive ports—GSM, BOFFA, and Konta—with a combined handling capacity of 16 million metric tonnes (MMT). It manages an internal road network exceeding 370 km and has built a 100-meter bridge to access rich deposits in the BOFFA region.

A strategic partnership with China Railway bolsters its mining, transport, and logistics capabilities. This setup is ideally positioned to feed the insatiable Chinese market, where domestic bauxite is dwindling due to environmental norms and depleting reserves. China imports roughly 200 million tonnes of bauxite annually, with imports growing at 10-15% each year, fueled by its clean energy transition.

The numbers reflect a successful scale-up: bauxite exports hit 3.38 MMT in H1FY26, nearly matching the entire previous fiscal year's volume. In Q2FY26 alone, exports doubled year-on-year to 1.33 MMT. Most sales to China are on a CIF basis, which includes freight and insurance, leading to higher revenue realization.

Ashapura plans to ramp up exports to 15 MMT by FY28. To support this, port capacity is being expanded from 16 MMT to 27 MMT by Q2FY27. Management describes this as a "linear progression," a deliberate, controlled increase in volumes.

Financial Surge and Future Diversification

The financial impact of this operational scale-up is already evident. For the first half of FY26, revenue jumped 75% year-on-year to ₹2,308 crore. EBITDA grew even faster, rising 105% to ₹320 crore, with margins expanding by 2.1 percentage points to 13.9%. Net profit skyrocketed 136% to ₹220 crore.

Looking beyond bauxite, Ashapura is diversifying its Guinea portfolio by entering the iron ore market. It has a long-term contract with a local plant and expects to commercialize around 1 million tonnes within the next few quarters. While structured on an ex-works basis (lower revenue but also lower logistics costs), it is expected to be an incremental profit contributor.

Despite the impressive performance, risks remain. The company trades at an EV/EBITDA multiple of 15, above its five-year median of 11, reflecting high growth expectations. Its fortunes are also tethered to bauxite price volatility and its concentrated dependence on Guinea for export volumes. The sustainability of its stock rally hinges on its ability to execute its ambitious expansion plans while navigating these global uncertainties.